- If you're considering a Roth individual retirement account conversion, your tax bracket could help you decide whether the move makes sense.

- Before completing the transfer, you need to know how long it will take to break even on upfront taxes, based on your long-term goals.

- You should also weigh other financial planning opportunities in lower-income years, experts say.

If you're considering a Roth individual retirement account conversion, your tax bracket could help you decide whether the move makes sense.

Roth conversions transfer pretax or nondeductible IRA funds to a Roth IRA, which can begin tax-free growth. The trade-off is paying upfront taxes on the converted balance — and you'll need a plan to cover that expense.

Typically, the strategy is popular during a stock market downturn because the converted balance triggers a smaller tax bill. Plus, investors can get more tax-free growth when the market bounces back.

More from Personal Finance:

That Roth IRA conversion comes with a tax bill — here's how to pay for it

Fed is likely to cut interest rates next week. Here's what that means for you

Egg prices may soon 'flirt with record highs,' supplier says. Here's why

Regardless of the timing, you'll owe regular income taxes on the converted balance, depending on your tax bracket.

It's important to know how long it will take to break even on upfront taxes, based on your long-term goals, experts say.

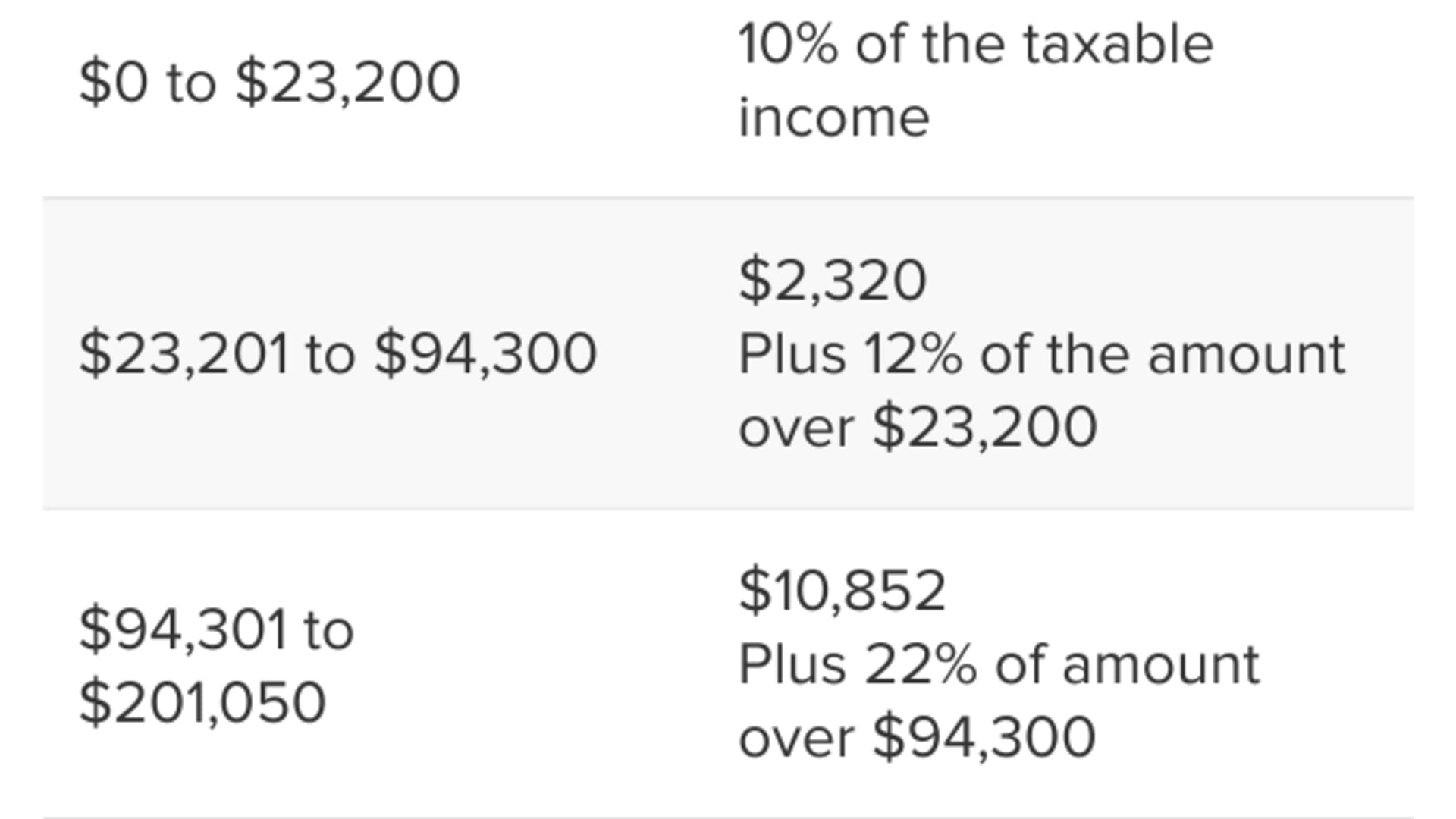

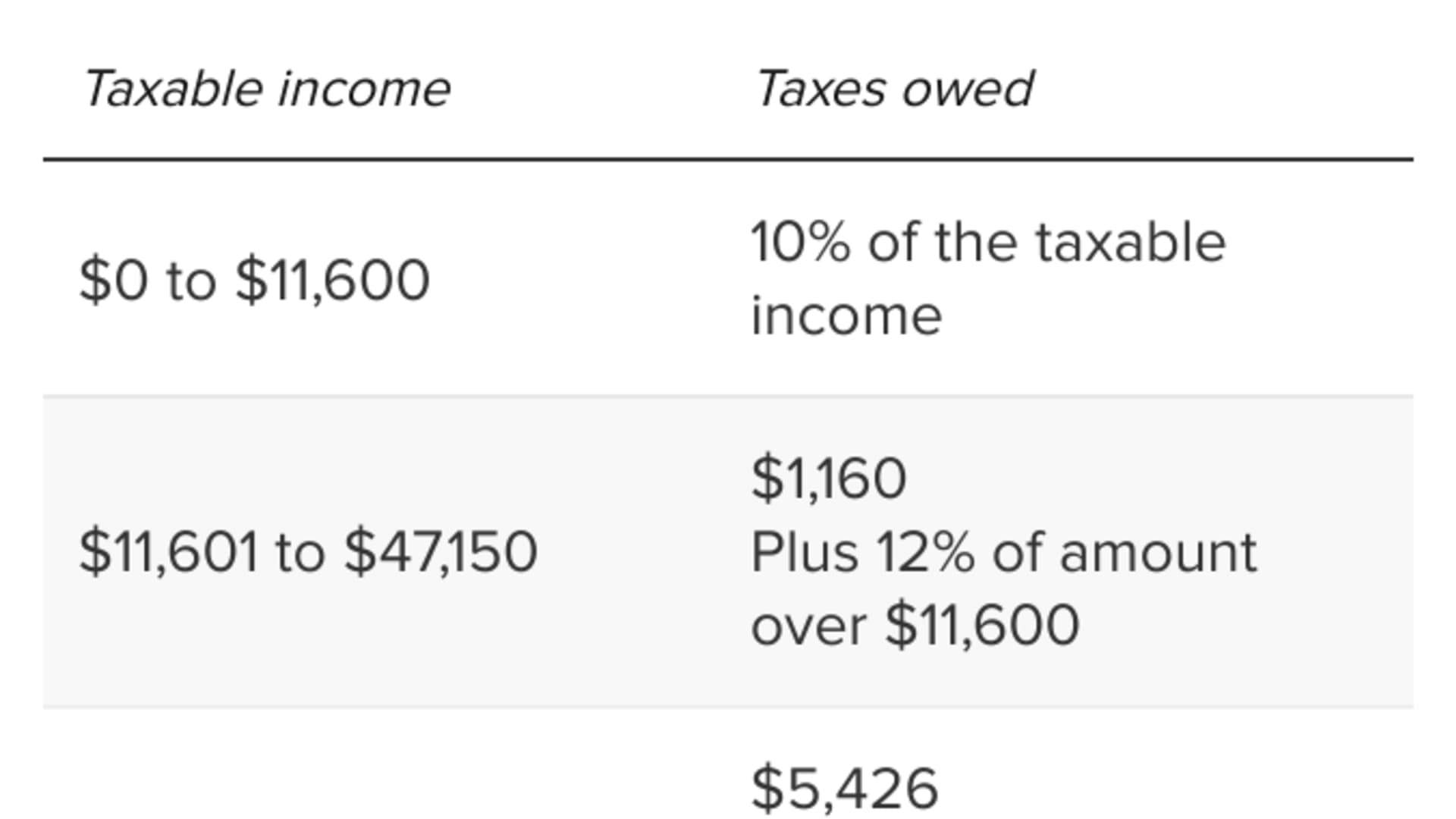

The best tax brackets for Roth conversions

Money Report

When crunching the numbers for a Roth conversion, you'll want to consider how the transfer impacts your current tax bracket, according to Tommy Lucas, a certified financial planner and enrolled agent at Moisand Fitzgerald Tamayo in Orlando, Florida.

If you can stay within the 12% tax bracket or lower, "that's a no-brainer, 99% of the time," he said. But anything above the 12% is "situational," depending on a client's goals and other factors.

Feeling out of the loop? We'll catch you up on the Chicago news you need to know. Sign up for the weekly> Chicago Catch-Up newsletter.

Ryan Losi, a certified public accountant and executive vice president of CPA firm Piascik, also uses a "rule of thumb" to greenlight Roth conversions.

"If we can convert and still stay in the 24% bracket or lower, I'm a thumbs up," he said. But bumping into the 32% bracket or higher prolongs the "recovery period" to recoup upfront taxes.

Of course, these benchmarks can change depending on a client's unique circumstances, such as estate planning goals, experts say.

Weigh rebalancing in lower-income years

When completing a Roth conversion, advisors typically aim to fill a specific tax bracket with income without spilling into the next one.

But you could miss other planning opportunities by focusing solely on Roth conversions, Lucas said.

For example, if you're sitting on a large brokerage account with sizable gains, you could leverage your lower tax brackets to rebalance your portfolio, he said.

The strategy, known as "tax gain harvesting" involves strategically selling profitable assets during lower-income years.

For 2024, you may qualify for the 0% long-term capital gains rate with a taxable income of up to $47,025 if you're a single filer or up to $94,050 for married couples filing jointly.

These figures would include assets sold from your brokerage account.