It’s time to boost 401(k) plan contributions for 2024. Here’s how much you should save

- Without action from Congress, trillions of tax breaks enacted by former President Donald Trump will expire after 2025, including lower federal income tax brackets.

- Higher brackets can impact "short-term capital gains," or assets owned for one year or less, in your brokerage account.

- You can minimize capital gain payouts by investing in assets like exchange-traded funds, experts say.

If you're investing in a brokerage account, it's important to know how assets can impact your taxes, especially with possible rate increases on the horizon.

Without action from Congress, trillions of tax breaks enacted by former President Donald Trump will expire after 2025, including lower federal income tax brackets, among other provisions.

Higher rates after 2025 could impact some brokerage accounts since investors pay annual taxes on earnings, experts say.

If you sell investments that you have owned for one year or less, the profits incur "short-term capital gains," or regular income taxes. The same rule can apply to mutual fund distributions, depending on how long the fund manager owned the underlying assets.

"Generally speaking, it's good to avoid short-term gains as much as you can," said Samantha Pahlow, wealth management chair of Ferguson Wellman Capital Management in Portland, Oregon, which ranked No. 10 on CNBC's 2024 FA 100 list.

Money Report

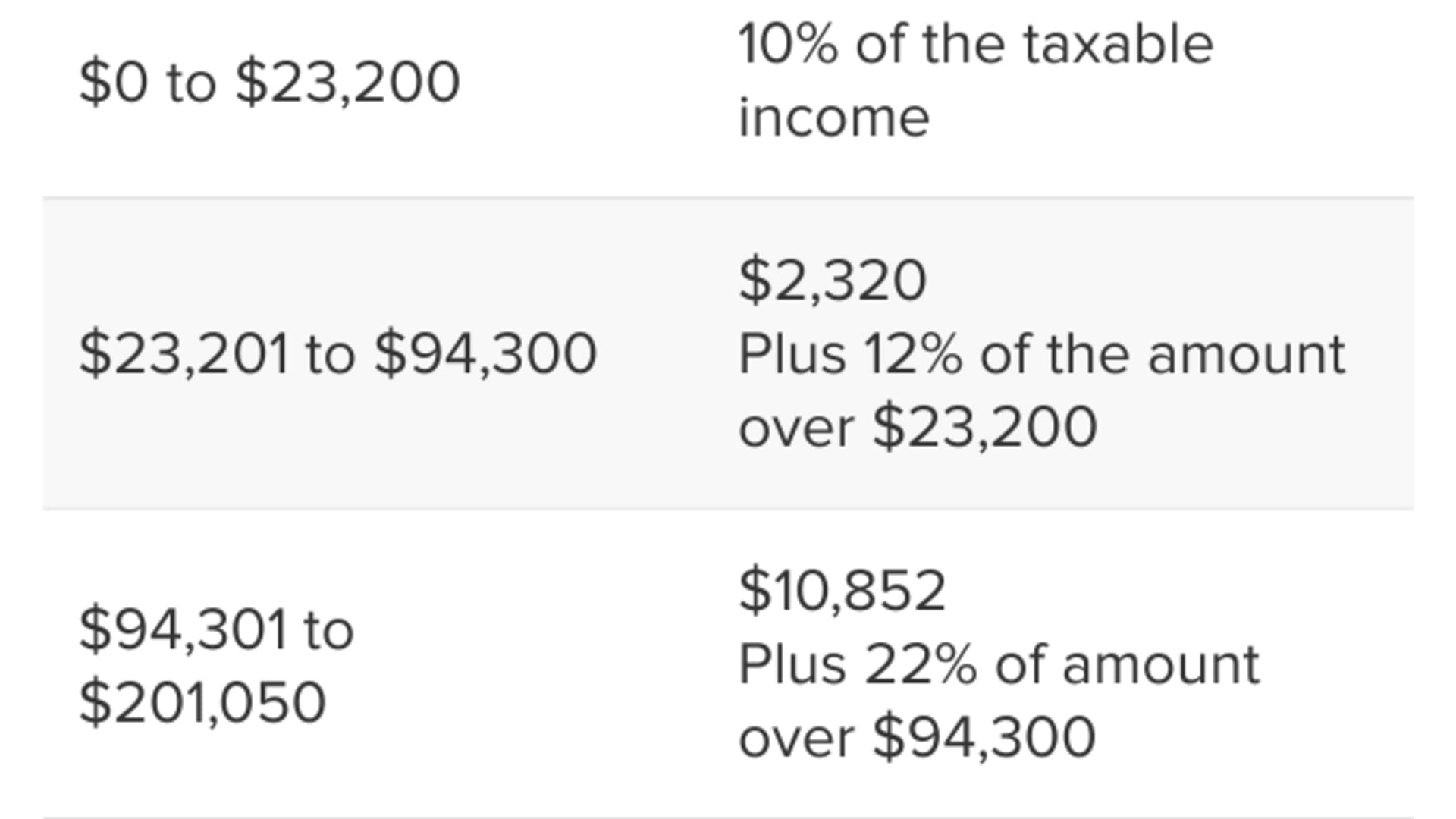

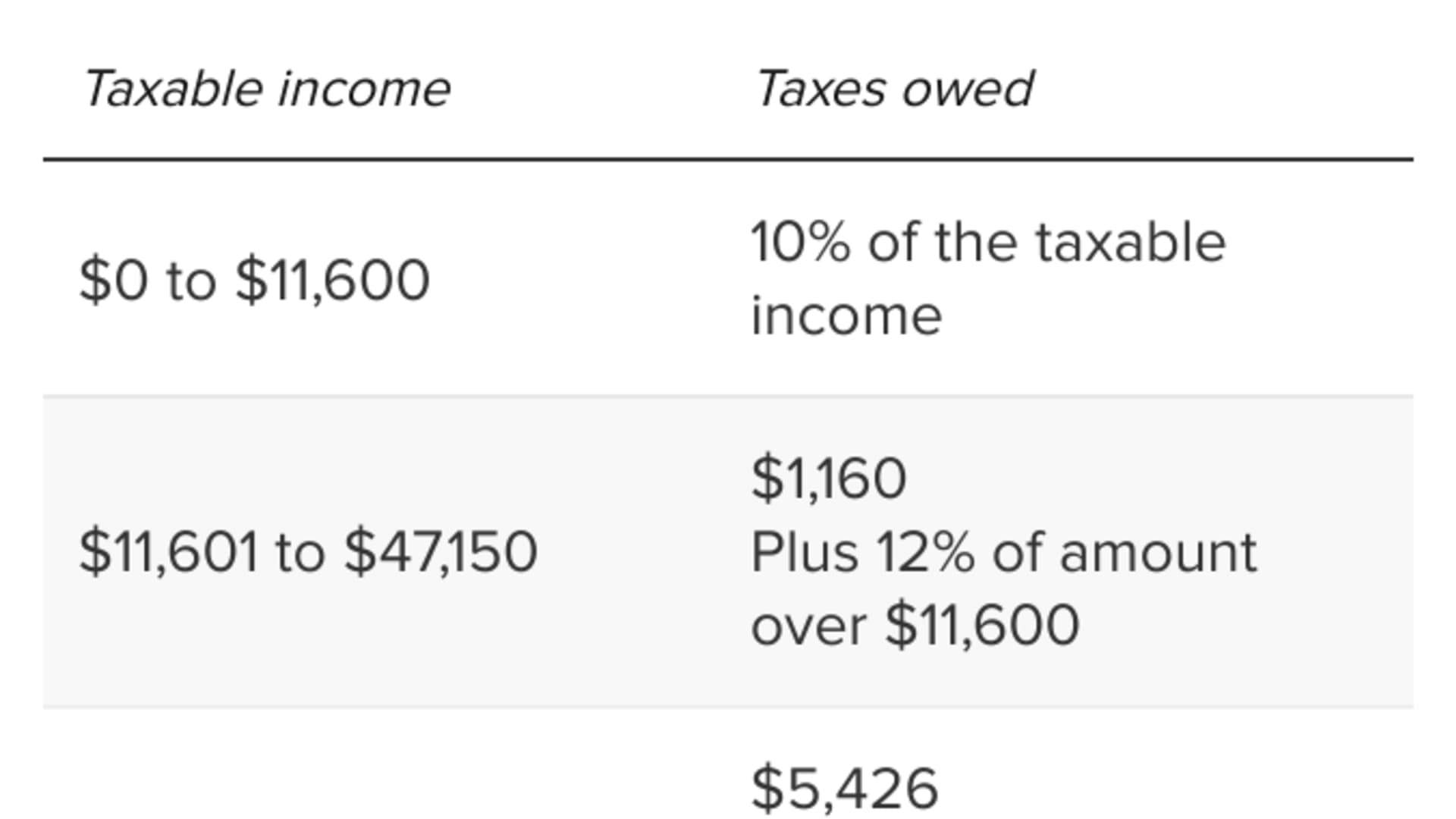

After 2025, short-term gains in a brokerage account could become more expensive, with brackets scheduled to revert to 10%, 15%, 25%, 28%, 33%, 35% and 39.6%, experts say.

But it's unclear whether Congress will allow lower brackets to sunset, particularly with control of the Senate, House and White House uncertain.

Feeling out of the loop? We'll catch you up on the Chicago news you need to know. Sign up for the weekly> Chicago Catch-Up newsletter.

Exchange-traded funds are 'more efficient' for taxes

Regardless of future tax law changes, investors should consider the types of assets they use in brokerage accounts, along with the possible tax consequences, experts say.

Exchange-traded funds "are certainly going to be more efficient than those actively traded [mutual] funds that may have very high turnover rates," said Shea Abernethy, a Winston-Salem, North Carolina-based investment advisor representative.

Actively managed mutual funds often trigger capital gains payouts, even when investors haven't sold shares, which can be a costly year-end surprise.

But minimally-traded funds, such as ETFs or index funds, typically offer more year-to-year tax savings, said Abernethy, who is also chief compliance officer for Salem Investment Counselors, which earned the No. 8 spot on the FA 100 list.

When aiming for tax efficiency, "mutual funds are kind of the dinosaur of the past," added Tommy Lucas, a certified financial planner and enrolled agent at Moisand Fitzgerald Tamayo in Orlando, Florida.

However, it's important to consider more than taxes alone before making an investing decision, experts say. Ultimately, your assets should reflect your risk tolerance, goals and timeline.